THE Mindanao Development Authority (MinDA) is pushing for more renewable energy facilities in this southernmost part of the country to keep with surging electricity demand driven by rapid growth of industries, real estate, services sector and agribusiness.

This was announced here by MinDA Assistant Secretary and Deputy Executive Director Romeo Montenegro to the stakeholders at the Water, Energy and Power Summit held on Tuesday, March 26, in Zamboanga City.

Montenegro said that Mindanao will require about 3,500 megawatts of new capacity between 2021-2030.

He said from supply shortfall resulting in long brownouts in 2011, Mindanao started having more than enough power by end of 2015 and currently it has supply excess following the entry of new power plants, but needing more by 2022.

However, he lamented that the entry of mostly coal-powered plants had resulted in the reversal of renewable energy-fossil energy mix.

He said Mindanao’s power energy mix in 2015 was 49 percent hydro, 14 percent coal, 31 percent oil-based and six percent geothermal, or 55 percent renewable energy and 45 percent fossil.

He said that in 2017, it was 49 percent coal, 29 percent hydro, 18 percent oil-based, three percent geothermal and one percent biomass or 67 percent fossil and 33 percent renewable energy. (Bong Garcia/SunStar Philippines)

ENGIE has teamed up with a Myanmar-focused off-grid energy specialist to help spur rural electrification across the Southeast Asian country with mini-grids combining PV, diesel and battery storage.

The French energy giant has been increasingly active in the off-grid clean energy space in India and Africa since 2016, and this month has taken a minority stake in Mandalay Yoma Energy, to focus on Myanmar’s national programme for total electrification by 2030, in a country that has at least 27 million people without access to power.

Nathalie Risteau, director and co-founder of Mandalay Yoma, told PV Tech that the company is already providing power to 6,000 consumers, which is more than half of what the government achieved in the last two years.

Hanoi (VNA) – Vietnam is one of the most efficient power markets in Southeast Asia, and has achieved nearly 99 percent electrification with relatively low cost in comparison to neighbouring country, according to the Ministry of Industry and Trade (MoIT).

The ministry shared the information at the Electrify Vietnam 2019 Conference held in Ho Chi Minh City on March 28.

According to Phan The Anh, deputy director of the MoIT’s Agency for Southern Affairs, power demand is forecasted to growth by more than 10 percent each year from now to the end of 2020 and by 8 percent annually during 2021-2030. Therefore, to satisfy the increasing demand, Vietnam will need 60,000 MW of electricity by 2020, 96,500 MW by 2025 and 129,500 MW by 2030.

The country has diverse energy sources, ranging from coal, oil, natural gas, hydropower, and renewable energy. At present, hydropower and coal-fired power lead amongst the power generation sources, and will continue to be the main short-term power sources for the country.

In the context of rising power demand, the Vietnamese Government has revised its power development plan in the direction of raising the power output from renewable sources. The Government also affirmed the importance of the stable and sustainable development of power sources in socio-economic development.

Nguyen Van Vy, Vice Chairman of the Vietnam Energy Association (VEA), said many foreign organisations are supporting Vietnam in assessing energy source development potential. Many investors have also expressed interest in the energy market in Vietnam, considering preferential treatment for investment in solar and wind power.

However, experts said new measures are needed to attract investment and improve energy efficiency from production to consumption in order to fully realise the country’s energy potential.-VNA

The government has said Indonesia will accelerate the mandatory use of 30 percent blended biodiesel ( B30 ) in anticipation of the European Union’s move to ban palm oil-based biofuel in its member countries.

Its mandatory use was set to take effect in 2020 but it was brought forward to September in response to the drafting of the EU’s Renewable Energy Directive (RED) II that was prepared by the European Commission. It is currently being debated by EU leaders.

Indonesian Oil Palm Estate Fund (BPDP-KS) head Dono Soestami said in Jakarta on Wednesday that the policy was needed because the country needed to expand the domestic market for palm oil and its derivative products.

“We will use B30 in September or October 2019, starting with 30,000 kiloliters or 50,000 kl. The most important thing is that we have to start,” Dono added as quoted by kontan.co.id.

Indonesia introduced the mandatory use of 20 percent blended biodiesel ( B20 ) in September last year and the government is also studying the possibility using B100.

With the mandatory use of both B20 and B30, the domestic market is expected to absorb 9 million tons of crude palm oil (CPO).

Last year, Indonesia exported 34.71 million tons of CPO from 32.18 million tons the previous year, according to the Indonesian Palm Oil Association.

Dono suggested that the green fuel program was expected to absorb some 25 million tons of CPO in 2025. He said without an effort to expand the absorption of CPO in the domestic market, the oversupply of the commodity would reach 55 million tons in 2025. (bbn)

JAKARTA — With every tree felled and every piece of coal burned for energy, Indonesia is inching closer to its ecological tipping point. And once it passes that point, the country’s economy will greatly suffer, leading to an increase in poverty, a higher mortality rate and lower human development.

That’s the conclusion of a new government-sanctioned report, titled “Low Carbon Development: A Paradigm Shift Towards a Green Economy in Indonesia,” which paints a grim picture of Indonesia’s future should it continue with its current development model.

But the report also asserts that Indonesia can have a much different future — one where its citizens are as wealthy as those of the Netherlands or Germany today — if it transitions to a low-carbon economic model.

Over the decades, Indonesia has exploited its abundant natural resources to feed a population that’s now ballooned to 260 million and fuel an economy that’s among the world’s 15 biggest.

This development model has taken a toll on the environment and public health. Large cities like Jakarta are choked with air pollution. Rivers like the Citarum in West Java are choked with filth. Iconic species like the Sumatran tiger and Javan rhino are teetering on the edge of extinction. The nation’s vast peat swamp zones emit vast quantities of toxic haze due to large-scale drainage and slash-and-burn practices to make way for plantations. They also emit massive amounts of carbon, helping catapult Indonesia to become the fourth-largest greenhouse gas emitter in the world.

The report, sanctioned by the Ministry of Development Planning and a part of the ministry’s initiative to usher in a low-carbon development model, predicts that if Indonesia continues exhausting its natural resources and polluting the environment at the current rate, economic growth will start to gradually decrease beginning in 2019.

This would result from a decrease in the quality of environment, pollution, and scarcity of resources, which would also have a profound impact on mortality rate, leading to 40,000 more annual deaths per year.

The unemployment rate would rise from about 4.1 percent in 2017 to 6.9 percent by 2045, partly due to the health impacts of pollution and environmental degradation, which affects the employability of people of working age.

In addition, there would be a greater pressure on energy needs, leading to increases in price and decreases in productivity.

The cumulative losses of income would be $130 billion over the period 2019-2024, slowing down Indonesia’s annual economic growth to 4.7 percent by 2045, leading to over 1 million more people living in poverty — “a very troubling scenario,” the report says.

“Indonesia is in a position where it can avert further environmental damage by not following the experience of countries such as China, which have polluted and degraded their path out of poverty and into higher income categories,” the report says.

Mari Elka Pangestu, a commissioner of the ministry’s low-carbon development initiative, said the report should serve as a wakeup call for Indonesia to immediately transition away from its current development model and onto a more sustainable path.

“Don’t wait until we become like Beijing or New Delhi,” she said at the launch of the report in Jakarta. “It’s not until they can’t breathe [fresh air] that they start pressuring their governments to change. Let’s be ahead of the curve. Before we can no longer breathe, before we lose our islands, let’s start now.”

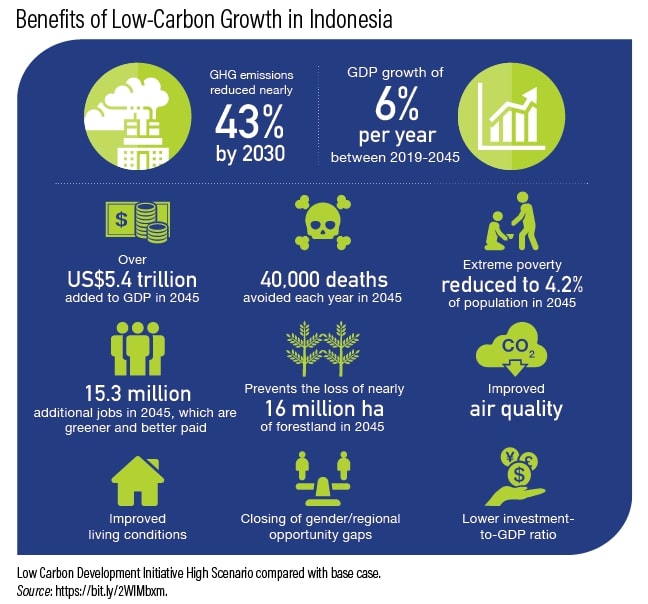

A list of benefits that Indonesia could reap if it transitions into a low-carbon economy. Image courtesy of Bappenas.

A different path

The report lays out its argument for how, should Indonesia adopt a low-carbon development model, it will reap benefits that are both immediate and long lasting.

Through 2024, Indonesia will enjoy an economic growth rate of 5.6 percent, which would further grow into 6 percent through 2045.

As a result, over $5.4 trillion will be added to its GDP in 2045. Its income per capita, which is currently lower than the world’s average, will balloon to nearly $17,000 by 2045, placing the country squarely in the group of developed economies.

Some of those predicted gains by 2045 stem from: 15.3 million additional, good-quality jobs, which are greener and better paid; extreme poverty halving to 4.2 percent of the population relative to 2018; about 40,000 lives saved every year from reduced air and water pollution; and the preservation of nearly 160,000 square kilometers (61,776 square miles) of forests that would otherwise have been cut down — an area larger than England.

Additionally, air quality and living conditions will have vastly improved, and the opportunity gap between women and men, and between provinces, will have diminished.

And due to less reliance on high-carbon economic activities, Indonesia will be able to slash its greenhouse gas emissions nearly 43 percent by 2030, surpassing its climate target of reducing between 29 percent and 41 percent of emissions depending on foreign assistance.

The report acknowledges that transitioning to a low-carbon economic model will require a dramatic overhaul of how the country manages its natural resources and meets the energy demands of its citizens.

For one, Indonesia would have to move away from coal and increase the share of renewable energy in the power sector to at least 30 percent by 2045. The report says renewable energy is now cheaper than coal in Indonesia when the externalized costs of air pollution are taken into account.

“Indonesia’s continued reliance on coal is built upon a now-outdated perception that the cost of coal is lower than alternative sources of energy, along with a set of political economy considerations,” the report says.

Furthermore, Indonesia has to reduce energy intensity (units of energy per unit of GDP) by 3.5 percent in 2030, and by 4.5 percent afterward.

To feed its growing population, the report continues, Indonesia should focus on increasing its land productivity by 4 percent each year, enabling its farmers to grow more food for more people using fewer resources, instead of on clearing more forests.

In fact, Indonesia needs to fully enforce existing moratoriums on forest clearance, oil palm expansion, coal expansion and peatland development as well as reforesting more than 10,000 square kilometers (3,861 square miles) of land per year by 2024.

If Indonesia manages to do so, by 2045 it will still contain 411,000 square kilometers (158,687 square miles) of primary forest, and nearly 150,000 square kilometers (57,915 square miles) of peatlands.

“Of special interest are primary forests, such as those in Papua and Kalimantan, and key [peatlands] and mangrove systems that support biodiversity, enhance resilience and contribute to carbon emissions reduction targets,” the report says.

Lastly, Indonesia will have to meet existing national and international targets for water, fisheries and biodiversity conservation.

A Sumatran tiger (Panthera tigris sumatrae) yawning. The population of Sumatran tiger has been pushed out of their forest habitats by rampant deforestation and hunting. Image by Rhett A. Butler/Mongabay.

A reliance on coal

Observers say all these talks about transitioning to a low-carbon economy would mean nothing if the country couldn’t end its coal addiction.

Currently, Indonesia still relies on fossil fuels to power its economy, with coal generating 58.6 percent of electricity, followed by gas with 22.5 percent, oil with 6.2 percent. Renewable energy only accounts for 12.7 percent of electricity.

While the government has set a target to increase renewable energy portion to 23 percent by 2025, it has also planned to continue relying on coal for foreseeable future in order to meet its ambitious target of adding 35,000 megawatts of power generation to the national grid over the coming years.

Recently, Energy and Mineral Resources Minister Ignasius Jonan said coal-fired power plants would still dominate the country’s electricity supply at 54.6 percent in 2025, even higher than the government’s previous plan.

The government even revived some coal power plant projects, namely the PLTU Java 5 and Java 9-10 projects. The projects had previously been eliminated from last year’s electricity procurement plan (RUPTL), but they reappeared in this year’s plan, despite warning from environmentalists that they will cause massive pollution.

“[In] terms of planning for additional generation capacity, the RUPTL remains anchored in old technology and is overly reliant on fossil fuels,” the Institute for Energy, Economics and Financial Analysis (IEEFA), a think tank, said in an analysis.

Environmental advocates, therefore, are skeptical that the transition to a low-carbon economy will happen, seeing how a coal power plant will remain in operation for at least four decades once it starts operating, locking Indonesia in a high-carbon economic development.

“If the government truly wants to transition, then it should’ve stopped the 35,000-megawatt project, especially those that still rely on fossil fuels and coal,” Even Sembiring, the policy assessment manager at the Indonesian Forum for the Environment (Walhi), told reporters.

He added that the next five-year development plan should include a mechanism to review projects that could hinder the transition process.

“The development plan should regulate how many permits should be evaluated in a certain year and how many coal should be reduced,” Even said. “But with the 35,000 megawatts project, the government instead builds energy infrastructure that relies on coal. That just doesn’t make any sense.”

Medrilzam, the head of the environmental department at the planning ministry, known by its Indonesian acronym Bappenas, admitted that the government’s plan to build more coal-fired power plants would make it more challenging for Indonesia to transition.

“When it comes to coal, it’s impossible to phase it out in a matter of five years because the contract [for coal plants] is a long term one,” he said. “There’s no way we can fully ditch coal, not even by 2045.”

Therefore, Medrilzam said the least the government could do was to manage the demand for electricity by promoting things like electric vehicles and biofuels.

“If the coal projects are already included in the electricity procurement plan, then we’re stuck,” he said. “That’s why, the only option for us is to manage our electricity demand.”

Medrilzam added that some people and businesses— especially those that rely on high-carbon sectors and resource extraction— would be negatively impacted by the shift to a low-carbon economy.

“There must be a trade off,” he said. “That’s why the shift will be gradual. Those affected will be given time to adjust their business model. We have to give ample time for them to shift their investments.”

A peat swamp in Sumatra smolders during the 2015 haze crisis. The drainage canals were dug in order to prepare the land for planting with oil palm, but the practice renders the land vulnerable to catching fire. Image by Rhett A. Butler/Mongabay.

False dichotomy?

Bambang Brodjonegoro, Indonesia’s minister for national development planning, said the report should put an end to the longstanding debate between environmentalists and business interests.

For decades, environmental advocates have been arguing that exploiting natural resources poses severe risks to the climate and the environment.

Businesses counter that by saying that jobs will be lost and the economy will suffer if the exploitation of natural resources are subject to exhaustive environmental regulations and review.

The debate, therefore, has been reduced to a forced choice that pits the interests of the environment directly against the interests of the economy.

“The low-carbon development path can bridge these two camps,” Bambang said. “So we reverse [our mindset] from growing our economy and emitting greenhouse gas emissions to reducing our emissions while maintaining our economic growth.”

Lord Nicholas Stern, co-chair of the Global Commission on the Economy and Climate, said the report should serve as a map for a more sustainable future for Indonesia.

“The LCDI report provides proof that you can grow economy and generate more quality jobs while reducing emissions,” he said. “Low-carbon growth drives growth itself, the transition is a driver and it leads to a better health, job and investment value. In the short run and in the long run, this transition is the only growth pathway for Indonesia in the future.”

In order to make sure that the transition happens, the planning ministry will incorporate the report into the next mid-term development plan, which will become the country’s first green development plan.

The plan, which will succeed the current five-year plan that expires in 2019, will center on quantifying the country’s ecological resources and planning its economic development accordingly, to prevent the depletion of those resources.

“The low-carbon development initiative will become an integral part of the next five-year development plan, which we’re currently being finalizing,” Bambang said. “The point is that we have to do it in the next five years.”

Given Indonesia’s outsized impact on the global climate, transitioning now to a low carbon economy will be good not only for Indonesia, but for the whole world, according to think-tank World Resources Institute (WRI).

“Perhaps just as important, other governments can learn from the country’s example,” WRI said in a blog post. “Indonesia’s new development plan is ambitious, yes, but it is also necessary, achievable and economically prudent. If Indonesia – an emerging economy with an imperative to improve its people’s standard of living – can pull off low carbon development, then other countries can, too.”

RENEWABLE energy sources can be just as – or even more – cost-competitive than conventionally generated power in South-east Asia, a study by the Asean-German Energy Programme has found.

“With a few years of development, solar PV (photo-voltaic) could potentially compete with conventional energy sources, especially if it was assumed that the prices of the conventional forms of energy will steadily increase,” the Asean Centre for Energy said in a report.

The Asean-German Energy Programme is a tie-up between the Indonesia-based centre and German development agency Deutsche Gesellschaft für Internationale Zusammenarbeit.

“Several factors, such as subsidies, resources scarcity, and the constant ageing of existing facilities will likely push the costs of conventional energy sources higher over time,” the report added. This is even though biomass and hydropower are the more cost-competitive renewable power sources for now, which the study attributed to the relative maturity of these technologies.

The latest study has found that hydropower sources in Indonesia, the Philippines, and Thailand could compete with conventional fuel generation, alongside most Malaysian projects. Some biomass projects in Indonesia, the Philippines and Thailand have also reached grid parity.

“However, with the cost of solar PV on a steeply declining trend, it could be a promising option for development,” the centre noted.

The analysis was based on the levelised cost of electricity, which measures the worth of electricity generation-related components, such as capital or operating costs, for each unit of power produced – in other words, the dollar value of each kilowatt-hour.

Solar PV has already reached grid price parity in Singapore and the Philippines, and if equipment costs can be brought down, solar energy could achieve this milestone in Thailand too, the report said.

The Asean Centre for Energy, which noted that the pace of renewable energy development in Asean is in line with global trends, called for targeted support from regional governments to address discount rates, capital costs and capacity factor, and thus spur renewable power development.

“For example, subsidies and financing mechanisms – that is, tax or land acquisition – could be created to reduce the capital costs,” it suggested. “Additionally, specific (renewable energy) research grants could be distributed to encourage technology production in the region and also efficiency enhancement.”

MANILA – Electric power supply remains an issue in the Philippines but officials from the public and private sectors said this may all change for the better when the country hosts two global power-related events within the next two years.

These events are the Association of Electricity Supply Industry of East Asia and the Western Pacific’s (AESIEAP) 2019 CEO Conference to be held in Cebu in September and the 2020 Conference on Electric Power Supply Industry (CEPSI) in Manila.

AESIEAP 2019-20 secretary-general Rogelio L. Singson, in a briefing at the Department of Energy (DOE), said they aim to exceed what was achieved when the country hosted the same events in 2000.

“We hope to repeat and even surpass what we achieved during our first hosting. We encourage all the members of the energy family to help secure this victory for our country,” he said, noting that past delegates are still talking about their experience during the country’s initial hosting.

In an interview with the Philippine News Agency, Singson stressed that even if the country has electricity supply issues this should not hamper it from showcasing what it can contribute for the industry.

“That’s the whole point. It doesn’t have to be that it’s only Singapore who can host. In fact, this is an opportunity to make everyone know the latest technology, (and) what are the solutions,” he said.

“This is a challenge for us hosting it but at the same time it is a good opportunity to have a good platform since all the latest technologies will be made available to our countrymen. Engineers can come, students can come and they will learn,” he said.

AESIEAP is the region’s largest organization of power and industry players.

The Department of Energy (DOE) will spearhead this year’s hosting, along with the Manila Electric Company (Meralco), the National Power Corporation (Napocor), the National Grid Corporation of the Philippines (NGCP), the National Transmission Corporation (TransCo), and the Department of Tourism (DOT).

The theme for this year’s event is “Energized Countries, Empowered Communities.”

More than 200 energy ministers and officials of power companies in AESIEAP member-countries are expected to attend the event at the Shangri La Mactan Resort and Spa from Sept. 22 to 25, 2019 while over 2,000 delegates are expected to attend the conference at the Philippine International Convention Center (PICC) from November 29 to December 3, 2020. (PNA)

JAKARTA, March 27 (Reuters) – A senior Indonesian minister warned on Wednesday Southeast Asia’s biggest economy could consider exiting the Paris climate deal if the European Union goes ahead with a plan to phase out palm oil in renewable transportation fuel.

Indonesia, the world’s biggest palm oil producer, has lashed out at the EU after the bloc classified palm oil as a risky crop that caused significant deforestation and ruled that its use in renewable fuel should stop by 2030.

Speaking at a palm oil forum, Luhut Pandjaitan, the coordinating minister overseeing maritime and natural resources, said the EU “should not underestimate Indonesia” and pledged the government would firmly defend its national interest.

Palm cultivation is often blamed for deforestation and destroying the habitat of endangered animals such as orangutans and Sumatran tigers.

Indonesia’s government, however, says palm requires far less land to produce oil compared to crops such as soy and rapeseed.

“If the U.S. and Brazil can leave the climate deal, we should consider that. Why not?” Pandjaitan said.

Under the Paris climate accord, Indonesia has committed to reducing its greenhouse gas emissions unconditionally by 29 percent and conditionally by 41 percent by 2030.

On Tuesday, the government said it plans to adopt sustainable economic policies which could help cut greenhouse gas emissions while boosting economic growth.

“The U.S. was not sanctioned at all by the EU (after leaving the Paris accord),” said Peter Gontha, special staff at Indonesia’s foreign ministry.

He also said Indonesia faced EU pressure over palm oil despite the government declaring a moratorium on permits for new estates.

Indonesia claims palm is being discriminated against by the EU to protect the market of European oils such as sunflower and rapeseed oils.

Indonesia has said it is preparing to challenge the EU and its Renewable Energy Directive (RED II) at the World Trade Organization as soon as it is implemented. The government is also examining its relations with EU members which support the act.

EU delegates for Indonesia and Brunei have said the bloc is complying with WTO rules and continues to be open for discussion with Indonesian government over the issue.

Earlier this week, and Indonesian Trade Ministry official urged palm companies to log legal action of their own over the issue at courts. (Reporting by Bernadette Christina Munthe, Fransiska Nangoy Editing by Ed Davies and Louise Heavens)